Last updated:

Introduction

The chances of success of the operation are increased if in period that precedes bond offering, the executive team of the potential issuer carries a solid end-to-end planning process.

Successful Bond Offering candidates will begin the adjustment process well in advance of the public launch.

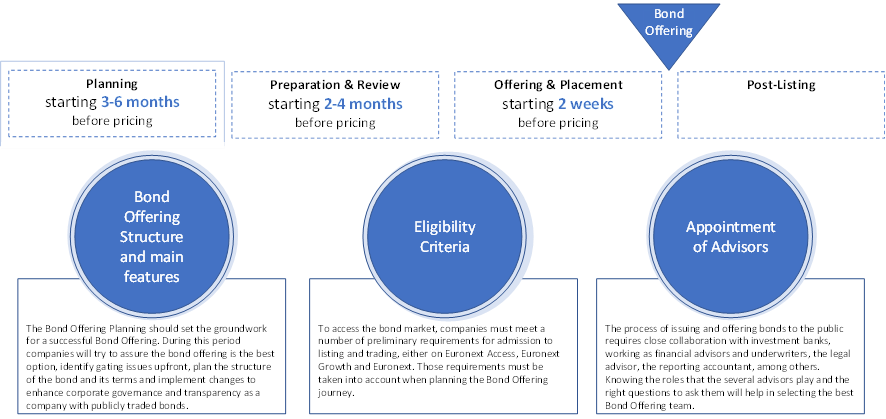

In the Planning phase, the main aspects to be covered are (i) Bond Offering Structure and main features; (ii) Eligibility criteria; and (iii) Appointment of Advisors. The following sub-chapters will cover each one of these (click on the diagram to fast-travel to any specific caption).

Bond Offering Structure and main features

Strategic Options

After pondering and evaluating alternatives, how to know if Bond Offering is the right strategy to achieve your goals?

While a Bond Offering may be your favored approach to raising funding, it’s still important to evaluate all possible funding options that could serve as attractive alternatives to a public listing in the context of shareholder and corporate objectives.

A detailed evaluation of the suitability and viability of other sources of debt, as an alternative to Bond Offering, should always form part of the process of determining whether to pursue a Bond Offering. Alternatives to ponder may include any combination of the following:

► Mezzanine debt

► Commercial paper

► Bank loans

► Private placement of corporate bonds towards Institutional and other qualified Investors

These alternatives and a comparative analysis between them is available in [X-Ref to the table presented in Chapter 2]

Given the range of potential alternative transactions, you need to have a clear idea of what’s involved, how long the process will take, what it’s likely to cost and whether two or more routes need to be run in parallel.

What are the different types of corporate bond offers available?

When choosing to raise capital by means of a corporate bond issuance and offer, Companies may choose between pursuing a public offer or a private placement. Below we present the main differences of those types of offers:

| Public Offer | A public offering corresponds to the sale of company’s newly issued bonds to the general public (both institutional and retail investors). In general terms, public offers are offers of securities addressed, wholly or partially, to unidentified recipients. This type of offer often requires the preparation and publication of a prospectus approved by CMVM. | While it enhances the Company’ image and credibility, a public offer also implies further requirements and obligations. |

| Private Placement | A private placement is an offering where new bonds are sold directly to institutional investors. The offer may be performed along with an initial listing. In this case, an approved prospectus is not required, unless bonds are to be listed in a regulated market, and the Company will only need to prepare an Information document. | While commonly faster and less cumbersome, a private offer may result in lower visibility and liquidity. |

What do investors look for/value in a bond issuer?

Prior to inventing in a bond offer, investors will mainly focus on an Issuer’s credit rating (if any) and financial metrics (i.e. leverage and financial ratios), as well as, the Company’s strategy and growth prospects, which are elements also considered when attributing in a rating of the bond issuer.

The bellow characteristics will illustrate an ideal bond Issuer:

► A stable and resilient business model;

► An established and steady financial track record;

► A market-leading position and good growth predictions;

► An experienced and skilled management team with a proven track record;

► A sound and healthy balance sheet;

► A strong cash generation, and the potential of future debt-deleveraging.

| Credit Rating | ► A credit rating refers to a quantified assessment of a borrower’s creditworthiness in general terms or with respect to a particular debt or financial obligation. Accordingly, the credit rating determines the ability of a company to fulfill its financial obligations within the defined deadline (i.e. likelihood a company will default or the credit risk carried by a debt instrument). ► Credit assessment and evaluation for companies is performed by a credit rating agency. These rating agencies are paid by the Company looking for a credit rating for itself or one of its debt issues. A credit agency appraises the credit rating of a debtor by evaluating the qualitative and quantitative attributes of the Company in consideration. The information used in the referred appraisal may be obtained from internal information provided by the Company, such as audited financial statements, business plan, annual reports, as well as external information such as published news articles, analyst reports, overall industry projections and analysis. ► A credit agency is not involved in the offering process, therefore, is considered to deliver an independent and unbiassed opinion of the credit risk carried by a specific company looking for to raise financing through a bond issuance. |

Additionally, investors will also have into account what is the intended use of the proceeds (e.g. acquisitions, refinancing of existing loans or general corporate purposes), and what collaterals and guarantees can be offered.

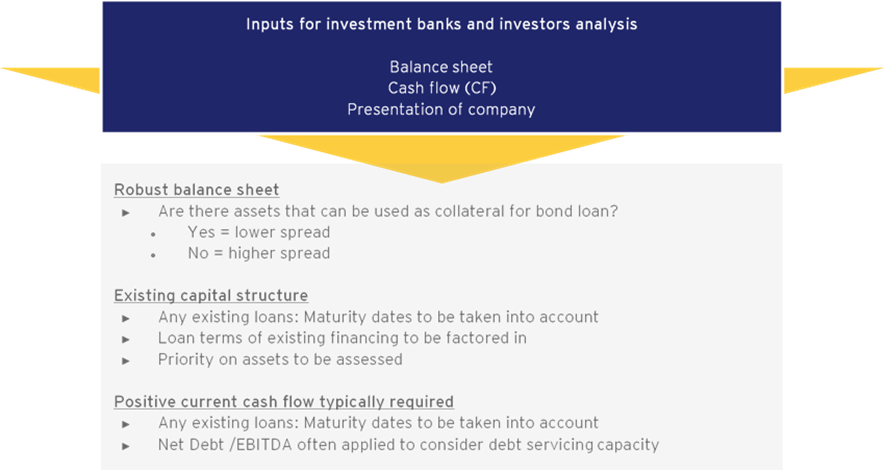

Usually, if a company wants to issue a bond it will request the assistance of an investment bank to place the offer. The diagram bellow presents an overview of the typical considerations the investment bank will make, when assessing the financial metrics of the Company at the start of the offering process. The terms and pricing of the bond to be issued will be subject, to some degree, to negotiations between the issuer and the investment bank.

Is your company suitable to proceed with the issuing?

Prior to embarking on a bond issue, the Company/Issuer must validate that there are no legal barriers to the issue. Accordingly, the issuer should check that:

► The issuance is compliant with the Issuer’s articles of association.

► There are no borrowing limitations in the Company’s articles of association or in contracts and agreements to which the Company is a party that could hinder the issuance.

Additionally, if the bond issue is to be guaranteed by a parent company of the Issuer, similar questions need to be addressed in relation to the guarantor.

Structuring the bond

In the planning phase of a corporate bond offering, the Company should consider various factors when structuring the bonds to be offered. Examples of such factors are presented below:

Size of the issue

The Company will typically have a notion of what amount of financing it will require for the planned investment. Nonetheless, when considering a bond issuance, companies need to have into account that the ticket size will impact the investors potential interest in the offering. Accordingly, smaller issues will mean fewer investors and hence less trading, and therefore low liquidity in the secondary market.

Additionally, is worth noticing that Institutional Investors, typically have interest in large ticket size investments and may not have mandates to invest in smaller bond issues.

Finally, as a bond offering entails higher costs when compared to the traditional bank loan and part of them are fixed, the larger the size of the offer the greater the dilution of these costs will be.

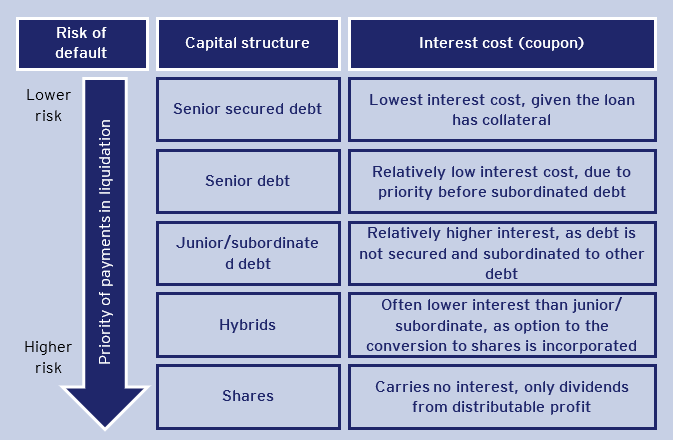

Capital Structure

The price and terms of the bond issue will be impacted by how the bond financing fits in with the Issuer’s existing capital structure. The Company must also deliberate what (if any) safety can be provided, which could offer lower interest costs. Typically, the best collateral has already been used as security for senior secured debt, while bond financing frequently is added on next. Bond debt will frequently rank behind secured debt with respect to security. Subordination (meaning that the debt ranks below other debts with regard to claims on assets or earnings) will let the Company to incur on further debt more cost-effectively. High-yield bonds will often be issued after existing debt, with less to no security and therefore with a high interest rate (coupon). A possibility to reach a lower interest rate can be to issue convertible bonds, as the investors will be rewarded with conversion rights in addition to the coupon (i.e. interest).

Additionally, the Issuer must also take into account the Company’s existing debt, given it may impact the ability of the Company to fulfill with its responsibilities. Furthermore, any loan agreements previously in place may have covenants that need to be considered when new bond financing is being planned. Financial modeling (which can be done with the assistance of financial advisors) can be applied to see how the several features of financing fits together, also taking into account the financial covenants of the respective senior debt, junior debt, convertible bonds and any future investment plans, transactions and so forth.

Bond Issuer

For Group companies it is necessary to decide which Company will proceed with the bond issuance. Given the bond purpose, the capital structure of the Company (or Group) and the existent debt, the bond Issuer can be the ultimate parent company, an intermediate holding/operating company or a lower-level operating company.

Typically senior debt is related to and secured by the operating Company(ies). Accordingly, this type of debt has lower risk for investors and can provide lower interest rates. On the other hand, high yield bonds are frequently issued by the parent holding company, with higher risk when compared to senior debt. When this is the case, the bondholders have no direct access to the assets of the operating companies (unless guarantees are provided). Sometimes such bonds are secured with share pledges in the operating subsidiaries, which, in case of a bankruptcy of the operating subsidiary, the bondholder’s claim as shareholders in the subsidiary (i.e. these claims will be subordinated to claims of all the creditors of the subsidiary).

Colateral and/or guarantees

To improve the terms of the bonds, a company may provide collaterals and/or guarantees. Assets can be used as collateral or shares in subsidiaries can be pledged as security. Alternatively, covenants can express that assets cannot be pledged without the consent of the bondholders (i.e. negative pledge). Additionally, to enhance the creditworthiness of the Issuer and improve the terms of the bonds, they can be guaranteed by the bond issuer’s subsidiaries. These guarantees will bring the bondholders closer to the assets of the Group and thereby avoid subordination.

In addition, further covenants may be included on the bond agreement to prevent the issuer from becoming excessively leveraged and preserve the assets of the issuer (or the Group), safeguarding the bondholders during the lifetime of the bonds. Accordingly, the covenant package may limit the ability of the issuer (or the overall group) to:

► Incur in additional debt;

► Distribute profits;

► Sell assets and subsidiary stock;

► Grant security interests on the assets;

► Provide additional guarantees;

► Enter into affiliate transactions;

► Execute mergers or acquisitions;

► Change the ownership structure of the issuer (or Group).

Maintenance covenants – A maintenance covenant requires the bond issuer to maintain a certain level of financial performance (measured with key financial ratios) to avoid default. Maintenance covenants are tested regularly. The Net Debt/EBITDA ratio and the interest coverage ratio are typical maintenance covenants. Another important covenant is the liquidity covenant, where the issuer (or group) needs to maintain a certain minimum of free cash. If such covenants are included in the bond agreement, the Issuer will need to have systems in place to monitor and forecast the financial development of the Company along the fulfillment of these covenants.

Incurrence covenants – Incurrence covenants are only triggered when the bond issuer undertakes some defined actions. For example, incurrence covenants can include that the Issuer is not allowed to distribute dividends, incur additional debt, proceed with M&A activities unless the relevant incurrence tests are met. Generally, executives find it easier to deal with incurrence covenants, given the Company will not need to continually monitor whether the financial ratios are maintained. Nonetheless, incurrence covenants offer lower safety for the bondholders, as they are only tested when the bond issuer undertakes specific actions.

Call and put options

To add flexibility to the bond and allow its early repayment the bond agreement can contain the possibility for the issuer to repay the bond loan prior to its maturity (call options). Accordingly, if advantageous, the issuer may repay the debt with excess liquidity, or refinance it with a loan with lower interest rate. Nonetheless, the use of call options will usually trigger a financial penalty, meaning that the issuer will have to redeem the bonds for slightly more than their face value.

The bond agreement may also include options for the bondholders for early repayment (put options).

The use of call and put options will be defined in the bond agreement.

Maturity and coupon

The Company should consider the maturity of the bond loan having into account its current future obligations (e.g. existing debt agreements) and its future cash flow prospects. Typically, higher maturities will require higher interest rates.

In addition the Company must decide the coupon (the fixed rate of interest that the bond issuer pays its bondholders). The coupon and the associated covenant package will reflect all factors set out above plus investor demand. Financial advisors will assist on the definition of those terms.

What debt products are available to list at Euronext?

| Standalone issuance vs. issuances under a program | A standalone bond issue is carried out independently, therefore, the issuer achieves a financing transaction in one shot, being relevant for a non-recurring need. The issuance is not integrated into a program unlike, for example, the case of a Medium-Term Notes program. Euro medium term note (EMTN) is a flexible medium-term debt instrument that is issued and traded outside of Canada and the United States, issued directly to the market with maturities of less than five years and offered continuously, instead of an all at once standalone bond issue. EMTNs make it easier for issuers to enter foreign markets for capital. With EMTNs, the issuer maintains a standardised document, also known as a program, which can be transferred across all issues and has a great proportion of sales through a syndication of pre-selected buyers. |

| Green bonds | Green Bonds enable capital-raising and investment for new and existing projects with environmental benefits. The categories of potential eligible green projects include, but are not limited to, renewable energy, energy efficiency, sustainable waste management, sustainable land use, biodiversity conservation, clean transportation, climate change and climate adaptation. All issuers that intend to issue a green bond must submit an independent third-party external review. There is no preference as to which framework will be used but, to be accepted, your report should be consistent with ICMA’s Guidelines for External Reviewers. To continue to be eligible for sustainable financing, issuers of green bonds must submit material information and reports regarding the current ‘ESG’ status of the bond(s) for filing. The issuer will provide the stock market with any information that may cause the ESG bond(s) to no longer qualify, as soon as the issuer becomes aware of such information. |

| Sustainability linked bonds | Sustainability-linked bonds aim to further develop the key role that debt markets can play in funding and encouraging companies that contribute to sustainability (from an environmental and/or social and/or governance perspective). Unlike Green Bonds, Sustainability linked bonds can be used to finance any corporate activity and their proceeds do not need to be allocated to specific projects. Notwithstanding, the issuer commits to reaching determined measurable Sustainability Performance Targets around pre-determined KPIs, and to having these reviewed by an independent external party. Another core feature of this type of bonds is that the financial and/or structural characteristics of the bond can vary depending on whether the issuer achieves the predefined sustainability objectives. |

Eligibility criteria

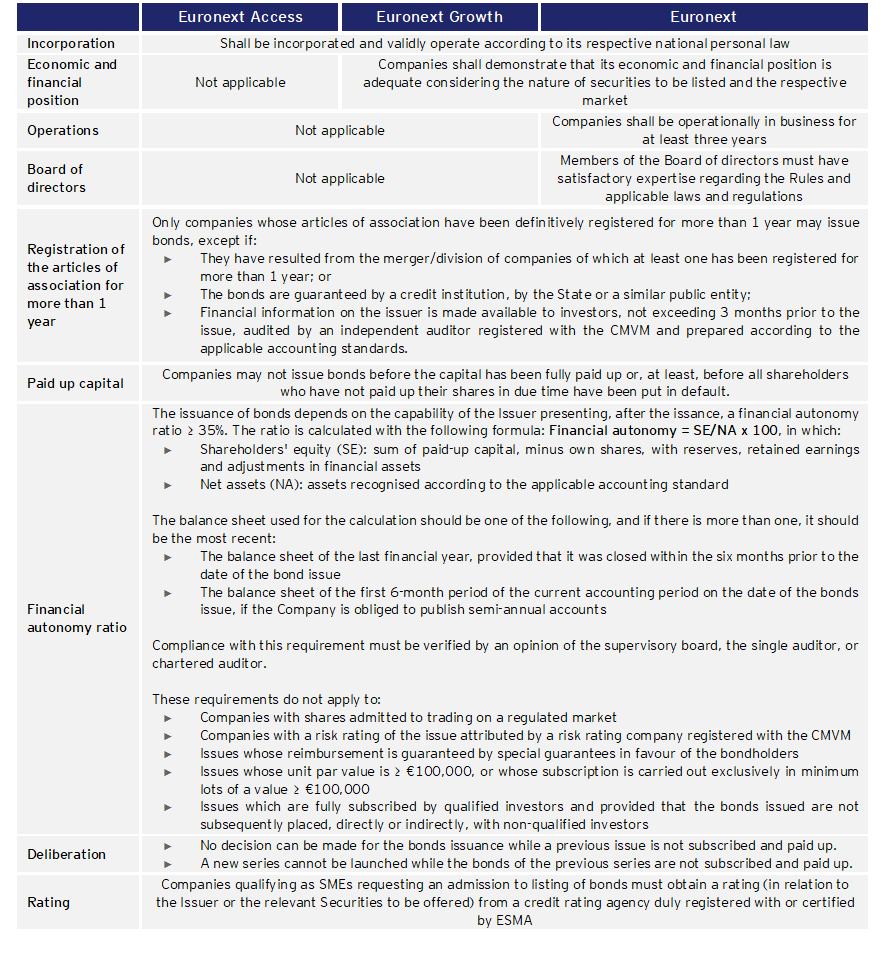

You should have to consider the eligibility criteria of the markets your company is considering listing its bonds.

The listing of bonds on the existing Portuguese markets – Euronext, Euronext Access, Euronext Growth – is subject to preliminary requirements, which are established/ruled by:

► The Securities Code and/or EU Regulations;

► The Securities Market and Exchange Commission (CMVM) approved regulations;

► The Euronext Rule Books.

| Eunonext Access + | The Euronext Access + is a dedicated segment that is only available for Equity Securities and closed-ended investment entities, therefore, debt securities are not traded in this market segment. |

Requirements for admission on each market are shown below:

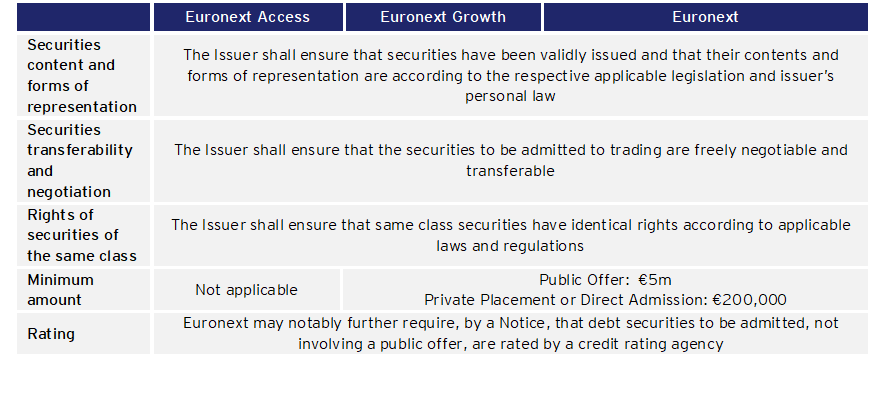

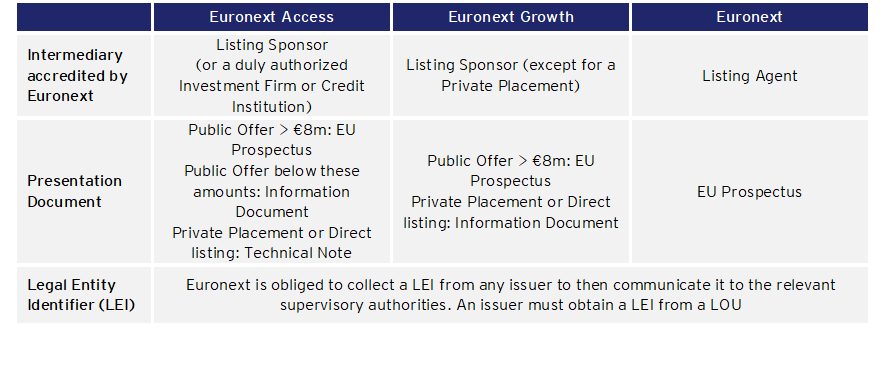

Issuer

| SMEs | Companies that have a market capitalisation of less than € 100 million (if listed) or according to their last annual or consolidated accounts meet at least two of the following three criteria: an average number of employees during the financial year of less than 250, a total balance sheet not exceeding € 43 million and an annual net turnover not exceeding € 50 million (if unlisted). |

Offered securities

Offer process

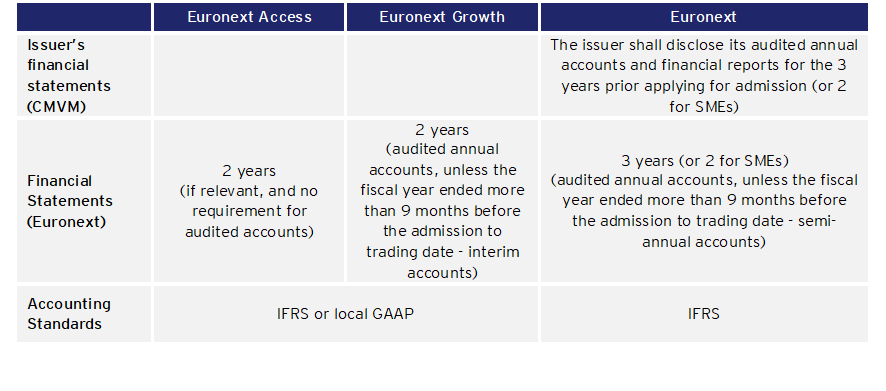

Financial information

Appointment of advisors

Do you know who to ask for assistance?

Besides the Company’s Management, investment banks/advisors will also have a crucial role in the Bond Offering process, by guaranteeing all the documentation for the offering is accurate and properly prepared, ensuring all the eligibility criteria is fulfilled, by managing the marketing and sale of the Company’s bonds to investors, and spending significant time analysing how to ‘‘position’’ the Company to achieve a successful offering. Therefore, an experienced and motivated team will increase the likelihood of an orderly and professional offering process and a positive reception from investors.

What factors should companies consider when selecting advisors?

| Track Record | Has the advisor been involved in successful Bond Offering processes? Does the legal advisor hold strong knowledge and practice in capital markets and industry specific legislation and regulation? |

| Reputation and Experience | Can the advisor provide special insights, advice, and research on the industry? Does the advisor have strong relationships with investors from the company’s industry? Is the advisor perceived as credible by the capital markets? |

| Analyst Coverage | Do research analysts cover the industry and comparable companies? |

| Distribution Strength | Does the advisor have solid distribution capabilities with retail and institutional investors? How effective is its retail sales force and its institutional sales force? Can the advisor reach regional, national or international? |

| Commitment to the Company | Will the advisor make the company’s offering a priority? |

| Aftermarket Support | Will the advisor continue to advise the company as a company with publicly traded bonds and, when applicable, present it to potential investors? |

The Company must dialogue with potential advisor candidates to measure how well they understand both the capital markets environment and, the Company and respective industry, and the aspects that investors will focus on in deciding whether to invest. To better decide between potential advisor, companies may test their knowledge regarding:

► Company’s comparables;

► The legal advisor should hold past experience in capital markets and industry specific legislation and regulation;

► How the Company’s bonds expected valuation compares to the comparables’ bonds valuation;

► Recent offerings have occurred in the Company’s industry;

► To what extent the pricing of the Company’s bonds will depend on historical earnings, future earnings projections, revenue trends and other factors;

► The pros and cons of each market segment to request admission to;

► What are the main steps the Company needs to take prior to the Bond Offering and how can the advisor help you.

TIP :

Advisors will certainly not want to commit significant time and resources if they are not confident that the offering will be successfully completed. The number of the advisors approached depends partly on the attractiveness of your offering. If it is large and likely to attract larger firms, you may decide to approach three or four financial intermediaries. It is important, though, to inform potential advisors that you are approaching others and to provide details about all features of your company and offering. If the offering is attractive, advisors will examine your company and sell their services to you.

Is a credit rating needed to proceed with an offering of bonds to the public?

According to Euronext Rulebooks, only companies qualifying as SMEs requesting an admission to listing of bonds via a retail offering / public offering are obliged to obtain a rating (in relation to the Issuer or the relevant Securities to be offered) from a credit rating agency duly registered with or certified by ESMA. “SMEs” means companies that have a market capitalisation of less than €100 million (if listed) or (if not listed) according to their last annual or consolidated accounts meet at least two of the following three criteria:

► An average number of employees during the financial year of less than 250;

► A total balance sheet not exceeding € 43 million; and

► An annual net turnover not exceeding € 50 million.

ESMA accredit credit rating agencies may be found on this website: CRA Authorisation (europa.eu). Currently there are three prominent credit agencies that control most of the overall ratings market: Moody’s Investor Services, Standard and Poor’s (S&P), and Fitch Group. Nonetheless, these bigger agencies are normally more expensive than the smaller ones. The credit agency that the issuer will choose will mostly depend on the target investor and how he perceives the agency. Accordingly, the issuer must choose a credit agency with enough credibility among its potential investors, which sometimes can be a smaller and less expensive entity.

Even if it is not mandatory to have a credit rating to execute the bond offering, Issuer’s may find it beneficial given some institutional investors may only invest on bonds with a rating attributed to it. Accordingly, having a credit rating may enhance the investors appetite for the offer.