Last updated:

Introduction

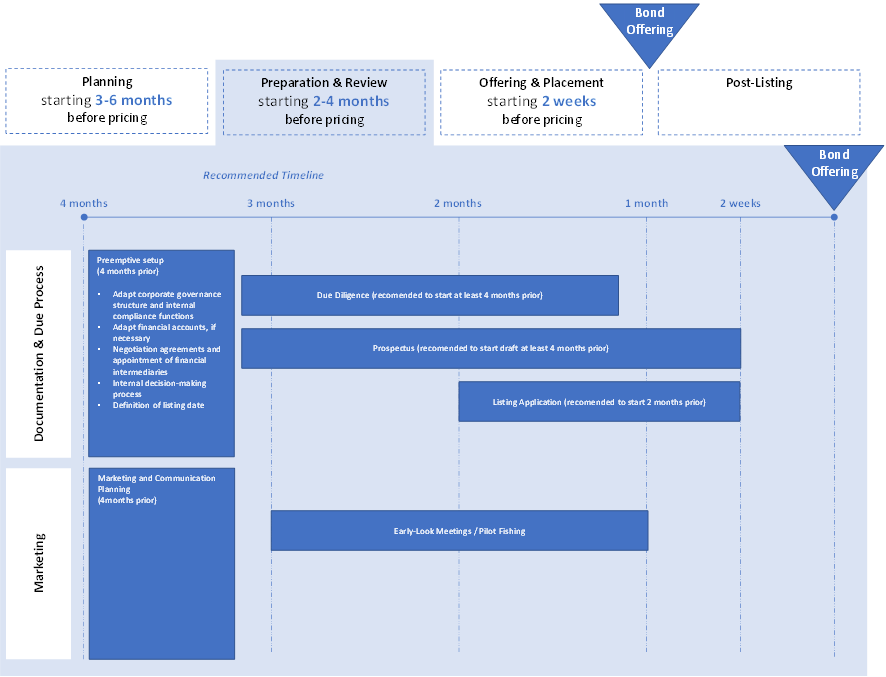

What are the necessary preparation steps you need to take?

Preemptive setup

Kick-off meeting

Once all members of the Bond Offering team have been selected, the kick-off meeting brings them together to agree on:

► Their roles and responsibilities;

► The offering’s nature and structure, namely, whether it will be made through (i) a public offering or also a private offering to institutional investors, (ii) an offering addressed to investors resident in Portugal or also to investors in other jurisdictions, and which ones;

► Coordination of responsibilities for drafting sections of the Prospectus;

► The timetable for the whole process; and

► The composition of the team member’s and workflows.

Adapt corporate governance structure and internal compliance functions

How efficient, compliant and accountable is your company?

Corporate Governance structure

Companies with bonds admitted to trading on regulated markets may have to adapt their organizational structure. Below it is presented the obligations that these companies must fulfill in what regards their organizational structure:

► General meetings – The General meeting table members of a company with securities admitted to trading on a regulated market, must be independent.

► Board of directors / Audit Board / Executive Board of directors / Supervisory Board – For the companies that have securities admitted to trading on a regulated market the liability of each member of the referred bodies must be guaranteed by one of the forms accepted by law, in an amount established in the articles of association, which may not be less than €250k.

► Audit Committee – For companies that have securities admitted to trading on a regulated market, the Audit committee must include at least one member who has a university degree appropriate to the performance of his duties and knowledge of auditing or accounting and who is independent.

***independent***

To be independent, the members must not be associated with any specific interest group of the Company or be under any circumstances likely to affect their exemption from analysis or decision. Particularly, to assure their independence, members cannot (i) hold or act on behalf of holders of a qualifying holding equal to or greater than 2% of the Company’s share capital; and (ii) have been re-elected for more than two terms, continuously or interspersed.

Review of internal functioning and organisation

In addition, the Company should also anticipate the rules that will have to comply after bonds are listed in order to allocate the necessary resources and put in place the internal compliance functions, processes and systems necessary to guarantee the compliance with those rules [For further information on this subject please see chapter 6. Life as a company with securities admitted to trading].

Adapt financial accounts, if necessary

A company with bonds admitted to trading on a Regulated Market, such as Euronext Lisbon, is required to report financial accounts in compliance with the accounting standards accepted at European level, corresponding to IAS/IFRS or accounting standards considered equivalent to IFRS by the European Commission. The Company will therefore have to consider the requirements and costs related to adoption of these accounting standards.

A company with bonds admitted to trading on Euronext Growth and Euronext Access has the choice of reporting its accounts in accordance with IFRS, or accounting standards considered equivalent to IFRS by the European Commission, or with the accounting standards applicable in Portugal (i.e. SNC).

Negotiation agreements and appointment of financial intermediaries

At the beginning of the Bond Offering journey the Company’s Management meets with potential Bond Offering partners that may be appointed to support the Bond Offering process and the Company on the life after becoming a company with listed bonds. Upon this process, the Company will celebrate the advisory contracts with the selected advisors to assist in the Offering.

One important partner may be the financial intermediary (i.e. financial advisor / investment bank) that will assure that the Bond Offering will be properly managed and successfully marketed. At this stage the Company will negotiate the placement agreement for the Offering. The signing of the contract will however take place at a later stage of the process, namely:

► Prior to the approval of the prospectus in case of a public offer; or

► On the day of Pricing, in case of a private placement.

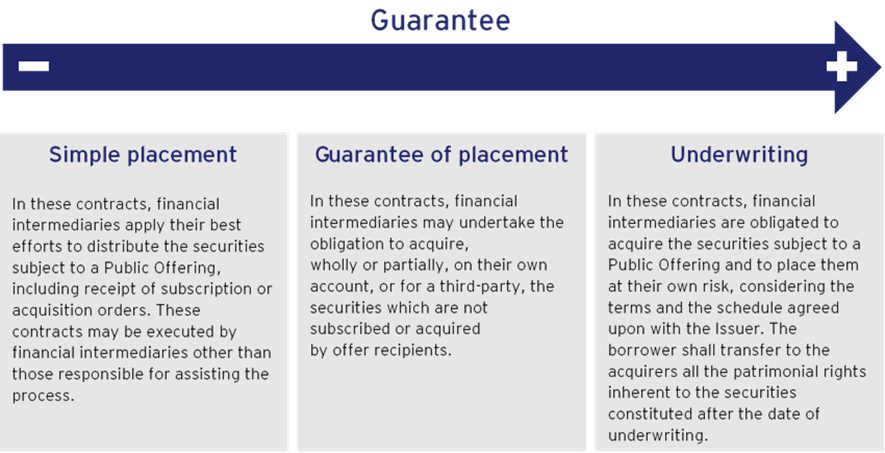

Placement agreements

A placement agreement is the contract, entered between an Issuer and a financial intermediary, or a syndicate of financial intermediaries, to regulate the terms and conditions of the distribution of securities that are the object of an offer.

Although the execution of a placement agreement is not mandatory in Public Offerings, having financial intermediaries assisting the Company in the distribution of securities in a bond offering will be a key for the success of the transaction. Please click below for further information on the type of placement agreements.

Internal decision-making process

Company bodies responsible for the Bond Offering decision

The decision to offering bonds to the public and related decisions during the bond offering journey require the prior approval of corporate resolutions during the Preparation phase, such as:

► Appointment of the Company’s advisors

► Decision to submit the listing application

► Decision to issue the bonds and structure of them (e.g. coupon payment periodicity, greenbond or not, etc.)

► Decision of allocation of bonds to the public offering and to the private offering to institutional investors (unless the bond offering only comprises the former)

► Pricing Decision

The Board of directors (or Executive Board) is generally responsible for the entire bond offering process and for the approval of the corporate decisions, except the bond issuance that requires the approval of the General Meeting (unless the Board is entitled by the Company’s by-laws to do so).

Engagement with the Regulator, the Stock Exchange and CSD

The applications for the prospectus approval by the Regulator (in Portugal, the CMVM) for the listing approval by the market operator (in Portugal, Euronext Lisbon) and registration of the Company’s bonds with the Central Securities Depository (in Portugal, Euronext Securities) should be filed with a set of legal and financial documents so that they are able to confirm that the Company complies with the applicable laws and regulations.

It is recommended that the Company, and its advisors, engage with these entities in an early stage of the Bond Offering journey for a smooth and timely approval procedure.

Due Diligence

Before a company requests the admission to trading of its bonds, it needs to take a number of preliminary steps. Firstly, a due diligence process must be performed, including close scrutiny of the Company’s financial, commercial, legal, accounting, tax and other affairs. This due diligence is conducted by the Company with the assistance of legal counsels and financial intermediaries, intervening in the placement and distribution of securities.

This process is intended to provide deep knowledge of the Company, allowing it to correct any problem or issue before the offering of its securities. This process also relates with the drawing process and publication of a Prospectus, since it ensures that relevant information about the Issuer is appropriately disclosed assuring the protection of investors given they will rely wholly on information disclosed in the Prospectus (for further information see the below section “5.1.2.3. Prospectus”). Throughout the Bond Offering process, additional due diligence sessions may be planned at each key milestone to ensure that information disclosed is up to date.

The results of this exercise will support the Company with the restructuring and strengthening of its corporate governance practices, as well as assurance of the completeness and accuracy of the information that will have to be provided and/or disclosed during the offering process.

Why should a Due Diligence be performed in the context of a Bond Offering?

The Due Diligence process is an essential step in the preparation of a Bond Offering, as it will bring to light the risks that may affect anyone who relies in the information contained in the Prospectus.

The purpose of conducting a Due Diligence process in the context of a Bond Offering is to:

► Select/identify the information that must be part of the Prospectus, to give the reader an accurate view of the potential investment, without misleading or deceptive statements or omissions.

► Test the assurance and accuracy of the information that will be included in the Prospectus. As a best practice, at the time the draft Prospectus is delivered, all information included in the Prospectus should be tied to a source document that was duly analysed during the Due Diligence and signed off by the Issuer’s board, management and external advisers (legal, accounting and any others as appropriate).

► Ensure that any risks and/or contingencies that were identified in the Due Diligence process are addressed/mitigated before the Offer opens to public investors.

► Document the investigation process, so that all the information that is ultimately part of the Prospectus has been validated by means of all reasonable inquiries and there is no relevant omission from the Prospectus in relation to that matter.

Prospectus

If you decide to proceed with a Public Offering of an amount higher or equal to €8 million and/or you will request admission of the offered bonds to a regulated market you will have to prepare and disclose to the public a Prospectus approved by the Regulator.

What is the Prospectus?

The Prospectus is a formal legal document, which provides to potential investors and analysts, all material key information that may affect the investment decision. The Prospectus includes legal, financial (both historical and prospective financial information) and commercial information with contents adapted to the Company’s profile and specific securities.

This document enables investors to clearly assess the Company’s patrimony, financial situation, results, and prospects. The Prospectus must be complete, understandable, and consistent. It must be published by the Issuer before an initial Public Offering approval by the Regulator.

The Prospectus may be drafted as a single document or as separate documents, dividing the required information into:

| Summary | The summary must be drawn up in a standardised format and in a concise manner, using simple language to make it easier to understand. The summary should contain key information regarding the risks of the Issuer and the securities that are being offered, the offer’s terms and conditions, detailed information on the admission to trading, and the reasons for the offer and the allocation of revenues. |

| Registration Document | Document presenting the Issuer, its sector and business activities, including risk factors, assets and liabilities, accounting and financial information, management, and corporate governance, among others. It contains all information that will subsequently be shared with investors and analysts through the media, ensuring fair and equal diffusion to all parties. |

| Equities Note | Document prepared by the Company and its advisors, defining the main terms of the transaction and information on the securities that are object of the request for admission to trading, including the number of bonds to be issued, the price range, the relative seniority of the securities in the issuer’s capital structure, the nominal interest rate and maturity date, a timetable for the subscription period, and the use of proceeds. |

What is an EU Growth Prospectus?

Considering the specificities of the different types of securities, Issuers, offers and admissions, the EU Prospectus Regulation has introduced different types of Prospectus, such as the EU Growth Prospectus. This is a simplified Prospectus for certain SMEs, making it easier and cheaper for these companies to access the capital markets and decrease administrative weight of the process. The EU Growth Prospectus may be used in case of a Bond Offering on Euronext Lisbon, Euronext Growth or Euronext Access.

In what context can a company choose to draw up an EU Growth Prospectus?

Companies which comply with the guidelines below can opt for the simplified EU Growth Prospectus, provided that they do not have securities admitted to trading on a regulated market:

► Companies, which can be classified as SMEs, i.e. according to their last annual or consolidated accounts, they meet at least two of the following three criteria:

i) an average headcount under 250;

ii) total assets recorded in the Balance Sheet do not exceed €43m;

iii) annual net turnover does not exceed €50m.

►Issuers, other than SMEs, whose securities are traded or are to be traded on an SME growth market, provided that those issuers had an average market capitalisation of less than €500m on the basis of end-year quotes for the three calendar years prior.

►Issuers whose securities total consideration in the EU does not exceed €20m calculated over a period of 12 months, and provided that such issuers have no securities traded on an MTF and have an average number of employees during the previous financial year which does not exceed 499.

What is EU passporting of Prospectus?

EU prospectus rules ensure that adequate and equivalent disclosure standards are in place in all EU countries so that investors can benefit from the same level of information. Under these rules, once a prospectus has been approved in one EU country, it is valid throughout the EU (single passport for the Issuers). This represents an important simplification for issuers since all the administrative procedures relating to the approval of the prospectus can be centralised with the financial markets regulator of the home country (in Portugal, the CMVM), without the financial markets regulator of the host country being involved in such approval.

Regarding the language regime for prospectuses, in cases where the passporting of a prospectus is to be requested, it must be drawn up in a language accepted by the Competent authorities.

Prospectus process

***1 – Preparation of the Document***

The occurrence of a Public Offering is preceded by the Regulator’s approval and the disclosure of an offering and listing Prospectus, encompassing complete, true, updated, clear, objective and lawful information necessary to enable the investors to make an informed judgement of:

► The characteristics of the offer, the corresponding securities and the rights thereto attached;

► The economic and financial position of the Company;

► The estimates regarding operating and financial activities and prospective financial information for both the Issuer and any eventual guarantor.

What information needs to be included in the Prospectus?

| Risk factors | The Prospectus must disclose all material risk factors that may affect the Issuer and its securities. These risk factors are usually identified during the Due Diligence process that is carried out as part of the preparation of the transaction. |

| Issuer’s financial data | The Prospectus must include the Annual Accounts for the last two financial years (or such shorter period as the issuer has been in operation). All historical financial information must be audited and certified by a Charted Accountant. Additionally, in case there is a material change (usually a transaction), additional financial information must be disclosed, namely, on how that event affected the financial position of the Company. |

| Alternative key performance indicators | Alternative key performance indicators may be provided when the items required to be disclosed do not give a clear picture of the Issuer’s performance or financial position. The Issuer shall clearly reconcile them with the financial statements, as well as explain their relevance and reliability. |

| Credit ratings | It must be disclosed, if applicable, credit ratings assigned to the securities at the request or with the cooperation of the issuer in the rating process and a brief explanation of the meaning of the ratings if this has previously been published by the rating provider. |

| Profit forecast | The Prospectus must include prospective financial information in the form of a financial performance forecast. |

| Tax information | The Prospectus must include a warning that the tax laws of the investor’s Member State and the Issuer’s Member State of incorporation may affect the income received on the securities. Additionally, the Prospectus shall include proper information in the case that the proposed investment originates a special tax regime, as for example in the case of investments in securities which give investors favourable tax treatment. |

| Offer price | It is allowed not to mention the final offer price and/or the final number of securities offered to the public, provided that: ► The prospectus discloses the criteria, and/or the conditions applicable in the determining the offer price and quantity of securities or, in the case of the price, the maximum price; or ► The agreement over either security purchases or subscriptions may be withdrawn for a period of no less than two working days following the filing of the final offer price and the quantity of securities on offer to the public. As soon as the final offer price and the final number of securities offered are determined, they must be notified to the CMVM and disclosed. |

Language

The Prospectus of public offers in Portugal are generally drafted in Portuguese, although the CMVM may accept it is written in English, with a Portuguese version of the Summary.

***2 – Submission and request for approval***

It is usual for the Issuer to enter into discussions with the Regulator preceding the formal submission of the Prospectus application. In Portugal, such discussions are mainly intended to properly define the procedure with the CMVM and to adopt, with its consultation, an indicative timetable including the Prospectus approval procedure. Given the short timeframe for approval of the Prospectus by the CMVM, these discussions are extremely important, and it is agreed that informal and updated versions of the draft Prospectus shall be regularly sent to the CMVM, to enable it to give enough advance notice of its observations and information requiring adjustments. For further information please access CMVM – Negociação / Emitentes / Operações e Informações.

***3 – Regulatory review***

The CMVM conducts a thorough review to verify the adequacy of the Prospectus with the legal requirements relating to its content and form, particularly by examining the completeness, comprehensibility and consistency of the content, and to ensure that the Prospectus contains all the information needed for investors to make an informed decision.

This review period starts when a first draft of the Prospectus is filed with the Regulator. Afterwards, through Q&As and revised versions of the document, the CMVM interacts with the issuer/advisors until every issue is solved.

***4 – Approval***

The approval of the Prospectus implies that it is complete, understandable and comprises reliable information. The CMVM will ensure that all the information contained in the Prospectus meets the minimum requirements to ensure that investors are able to make informed decisions about the securities.

Once the CMVM grants final approval, a press release announces the intention to float (ITF), disclosing the offering’s timing and details to the market, which kicks off the marketing (placement) phase.

What is the timing for the Prospectus approval?

Preliminary calendars are usually agreed upon with the CMVM so that the Company has some idea of when it can expect the competent authority to ratify the Prospectus.

Nonetheless, in accordance with the Portuguese Securities Code, the Issuer must be notified of the approval of the Prospectus, its registration or its refusal shall be informed to the offeror within eight days from the receipt of any complementary information required by CMVM.

***5 – Publication***

Upon approval, the final Prospectus version, stating the date of approval, must be published simultaneously on all selected platforms (see table below with the list of acceptable platforms), so it can be made available to the public. The prospectus must be made available to the public at a reasonable time in advance of, and at the latest at the beginning of, the offer to the public or the admission to trading of the securities involved.

Once approved, the prospectus must be made available to the public at a reasonable time in advance of, and at the latest at the beginning of, the offer to the public or the admission to trading of the securities involved.

Click on the button below to find out where the Prospectus must be published.

***button***

Where must the Prospectus be published?

The Prospectus must be made available to the public in electronic form on any of the following websites:

a) the website of the Issuer, the offeror or the person asking for admission to trading;

b) the website of the financial intermediaries placing or selling the securities, including paying agents;

c) the website of the market operator where the admission to trading is pursued;

d) the website of the Regulator who as approved the prospectus.

The Prospectus must be published on a dedicated section of the website which is easily accessible when entering the website. It must be downloadable, printable and in searchable electronic format that cannot be modified.

Validity

The Prospectus for a Public Offering for distribution remains valid for a 12-month period from the date of their approval by the CMVM, and provided the Prospectus is updated accordingly with any supplements or addenda that may be required.

Addenda and Rectifications

It may occur that in the time gap between the approval of the Prospectus and the date securities are admitted to trading (which usually coincides with the end of the offer period), an inconsistency is detected in the Prospectus. These inconsistencies may respect to:

► Detection of a significant omission, inaccuracy or mistake in the Prospectus; or

► Occurrence of a new fact, which may be relevant to the investors’ decisions.

In these cases, the Issuer/Offeror must issue a supplement to the Prospectus with the referred amendment/rectification and request approval of the document from CMVM.

Investors who accepted the offer prior to the disclosure of the addendum or amendment have the right to withdraw their acceptance within not less than two working days following the disclosure supplement, provided that the significant new factor, material mistake or material inaccuracy arose or was noted before the closing of the offer period or the delivery of the securities, whichever occurs first. That period may be extended by the Issuer or the offeror. The final date of the right of withdrawal must be stated in the supplement.

Listing application

In order for a Company’s bonds to be admitted to trading, a request for the listing of the bonds should be submitted to the Stock Exchange, who will verify compliance with the general requirements for admission to trading.

In case of listing in Portuguese markets, to kick-off the admission to trading process, the Issuer first meets with Euronext to present the listing project and agree on a timetable regarding the admission to trading process.

The Issuer must appoint a Listing Agent (Euronext Lisbon) and a Listing Sponsor (Euronext Growth and Euronext Access) who will assist and guide the Issuer with the admission to trading and also help the Company to prepare the application form and all the documentation that must be submitted to Euronext.

With the submission of the listing application, the Issuer and Euronext Lisbon should agree on a schedule for completion of the admission process.

At the same time as the proceedings above, the Issuer needs to register its bonds with the Portuguese Centralised System of Registration of Securities managed by Euronext Securities.

Upon registration, the bonds are assigned an ISIN code by Euronext Securities.

Decision

Euronext will decide on the application for admission to listing within a maximum period of 30 trading days (1 month for Euronext Growth and Euronext Access) of receiving the required documentation, unless agreed otherwise by the applicant company and Euronext Lisbon. In case of acceptance of the application, the decision must remain valid for a maximum period of 60 days.

Euronext will notify the Company of its decision, issuing a first market notice with the date on which the admission to trading of securities must become effective, the respective market, and any specific conditions related to the admission. Afterwards, Euronext may issue succeeding market notices relating to the admission to trading, confirming the conditions have been fulfilled, among other aspects. In the event of a Public Offering of securities, the admission to trading shall become effective only after the conclusion of the offering period.

Marketing and Communication Planning

The Issuer’s Marketing and Communication strategy throughout the Bond Offering process is crucial as it enables the Company to manage investor relations; generate interest and mitigate perceived uncertainty.

General considerations for Marketing and Communication in the Context of a Bond Offering

In the context of a Bond Offering, it is of paramount importance that the Issuer diligently defines how to present and promote the offer to potential investors. In a Bond Offering context, Marketing strategy has a great impact in managing investor relations; generating interest, mitigating perceived uncertainty and thus driving a higher price and defend from market turbulence. It is also relevant to mention that material information provided directly or indirectly by the Issuer and addressed to institutional investors or special categories of investors, including information disseminated at meetings relating to offers of investment instruments as well as information provided to financial analysts, shall be disclosed to all investors to whom the offer is addressed.

Until the offer is made public, all the parties involved in the offer need to:

► Restrict the disclosure of offer related information to that necessary to fulfilling the offer’s objectives and correspondingly warning addressees as to the privileged nature of the information issued.

► Limit the use of undisclosed information to purposes related to the preparation of the offer.

As from the moment of the offer is made public, all the parties involved in releasing information regarding the offer need to:

► Observe and comply with the quality of information principles;

► Ensure the information provided is consistent with the prospectus;

► Clarify their relationship(s) with the issuer or their interest in the offer.

Additionally, when conducting pre-offering marketing activities, all the parties involved in the Offer need to assure the compliance with the EU Market Abuse Regulation (“MAR”) in what respects disclosure of inside information the context of a market sounding.

MAR defines “inside information” as any nonpublic information of a precise nature relating, directly or indirectly, to an issuer or its securities and which, if made publicly available, is likely to significantly affect the price of the securities.

A market sounding comprises the communication of information to one or more potential investors, prior to the announcement of a transaction, in order to gauge the interest of potential investors in a possible transaction and its related conditions (e.g., potential size or pricing).

Click on the button below to find out more regarding the obligations that must be fulfilled in the context of MAR.

***button***

In a context of a Market Sounding, what are the obligations that have to be fulfilled?

A disclosing market participant must, prior to conducting a market sounding, specifically consider whether the market sounding will involve the disclosure of inside information and must make a written record of its conclusion and the reasons therefor and provide it to the CMVM upon request. This obligation must apply to each disclosure of information throughout the course of the market sounding, and so, the market participant must update the written records.

Before making the disclosure, the disclosing market participant must:

► Obtain the consent of the person receiving the market sounding to receive inside information;

► Inform the person receiving the market sounding that he is prohibited from using or attempting to use that information, by acquiring or disposing of financial instruments relating to that information;

► Inform the person receiving the market sounding that he is prohibited from using or attempting to use that information, by cancelling or amending an order which has already been placed regarding a financial instrument to which the information relates;

► Inform the person receiving the market sounding that by agreeing to receive the information he is obliged to keep the information confidential;

► The disclosing market participant must make and maintain a record of all information given to the person receiving the market sounding and must provide it to the CMVM upon request.

In the case where information that has been disclosed during a market sounding ceases to be inside information according to the evaluation of the disclosing market participant, he/she must inform the recipient accordingly, as soon as possible, and maintain a record of the information given and provide it to the CMVM upon request.

In the case of an offer of bonds being addressed solely to qualified investors, the communication of information to them for the purposes of negotiating the contractual terms and conditions of their participation in an issuance of these bonds by an issuer that has financial instruments admitted to trading on a trading venue, or by any person acting on its behalf or on its account, must not constitute a market sounding.

Such communication must be deemed to be made in the normal exercise of a person’s employment, profession or duties, as explained above (unlawful disclosure of inside information), and therefore must not constitute unlawful disclosure of inside information.

That issuer or any person acting on its behalf or on its account must ensure that the qualified investors receiving the information are aware of, and acknowledge in writing, the legal and regulatory duties entailed and are aware of the sanctions applicable to insider dealing and unlawful disclosure of inside information.

Early-look meetings with investors / pilot fishing

While the Prospectus is being drafted, a marketing strategy is designed to create investor interest and momentum. The Company and its advisors draw up a slideshow to use in meetings with investors and research analysts, which includes exclusively contents presented the Prospectus but, in a more appealing manner and directed to the target investors of such meetings.

The core marketing documents, such as the slideshow, the Bond Offering website, press releases and other communication materials, may all be adjusted throughout the Bond Offering process, up until the management roadshow, and are all carefully reviewed and subject to approval by the CMVM.

Meetings with investors

A best practice is to have an appointed communication agency setting up a training session agenda intended to prepare the Issuer’s Management for initial meetings with investors. These meetings are usually conducted by the CEO and include interventions by the CFO. The “pilot fishing” is done on a confidential basis and consists of these one-on-one confidential early-look meetings between Management and targeted investors, with the aim to introduce the Company on a preliminary basis by explaining its business model, to measure the initial market sentiment on the Company’s credit story, ask for the investors’ feedback on several matters, such as their perception of the Company, the Bond Offering and the bond coupon, to understand how the market will assess and value the bonds, and, most importantly, to create adhesion by investors. The management team must transmit confidence and persuade investors to trust the Company.

Pilot fishing allows an early assessment of the potential success of the Bond Offering. Based on the potential interest noticed at these meetings, which are spread out over time, the Company may adjust its Bond Offering project, and can postpone or even exit the process without a substantial financial commitment at this stage. If the meetings generate formal commitment of acceptance of the Offer, contractual orders will appear in the Prospectus, safeguarding pre-guaranteed demand from anchor and cornerstone investors.